Credit card companies know everything about you. In the era of big data, it’s financial institutions not Facebook that really strip your soul. You may not realise this, but credit card companies mine your purchase history to make some staggeringly personal deductions: whether you are gay or straight, how long your marriage will last, whether or not you have a junk food habit. Then they use it to determine credit scores, detect fraudulent behaviour or work out whether or not to bump up your health insurance premiums.

Opting out of the era of big data is nigh on impossible – as one academic recently discovered when she tried to keep her pregnancy a secret from online marketers. But those who want to maintain a little privacy may be interested to know that a South African company, Net1 Mobile Solutions, has come up with a way to at least keep some of your activities a secret.

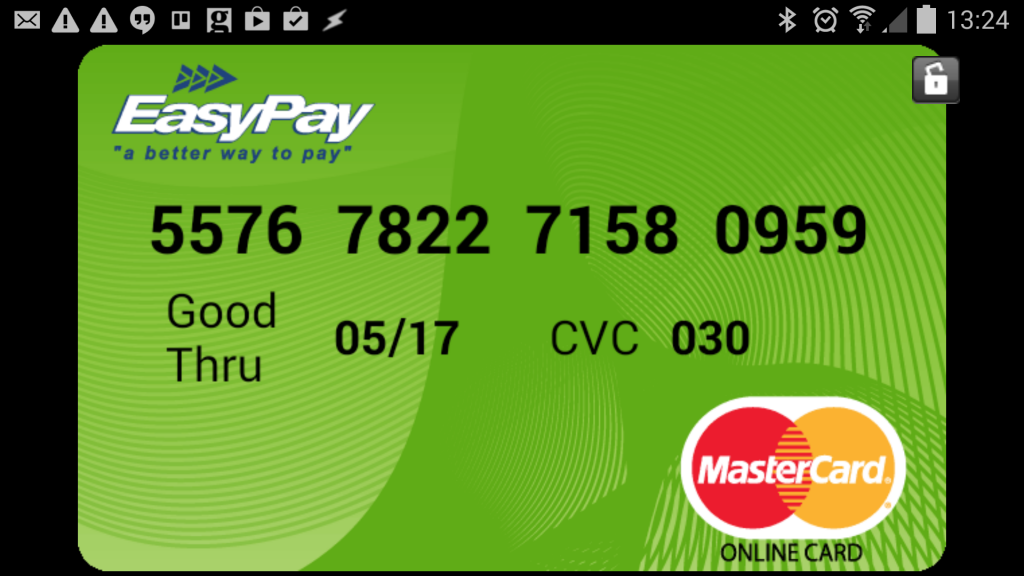

VCPay is a mobile app which can create single use credit cards that only exist on your phone screen. Once you’ve downloaded the app you’re given the option to either link it to an existing credit card or create a pre-pay account into which you can deposit funds via EFT. Then, when you need to pay for something, you create an instant credit card with working MasterCard details which appears on screen as an image.

The card can be used in one of two ways: either details can be copied into an online payment system or any other ‘card not present’ transaction, or – if you’re super modern – you can use it to pay at an NFC tap-and-go reader with a compatible phone.

As well as hiding what you’re actually buying from your credit card company, VCPay is arguably more secure too.

“We see a lot of big retailers getting hacked and losing credit card details,” says Net1 Mobile CEO Philip Belamant, referencing the recent security breach at US retailer Target in which 70 million customer records were hacked.“With VCPay if anyone gets those details, they’re useless.”

VCPay can actually create two types of card. As well as a single use card you can also create an “up to” card which functions like a normal credit card but self-destructs after it hits a predetermined limit. That way, if anyone does steal the details, your exposure to the amount potentially lost is limited to an inconvenience rather than a crisis.

“You don’t want to have to enter new create a new card every time you purchase a 99cent app on the App Store,” says Belamant, “So you might register an R500 card with Apple, for example.”

In addition, ‘up to’ card credentials can be revoked at any time. Belamant says that he sees this as useful for parents who want to give kids funds to buy a pair of shoes, for example, but are keen on getting the change back. Once a transaction of R700 goes through on an R1 000 card, for example, the card owner gets a notification and can pull the plug.

One particular South African use that springs to mind is topping up etoll tags – many people are reluctant to trust Sanral with their credit card numbers after multiple and highly critical security problems around the online billing service. A single use credit card, however, would take away the fear that someone else’s incompetence will lead to your bankruptcy.

And there are extra levels of security too: as part of its deal with the Grindrod bank to issue the card numbers, Net1 will underwrite losses on cards due to theft. And when a transaction is made on a single use card that needs to draw on a “real” card, your details only leave Net1’s servers as hashed entries for authentication – your actual entries are supposedly safe.

Net1 has similar relationships with Bankcorp for a US launch, and Access Bank in India.

While VCPay is of interest to those who want to maintain privacy, of course, it does come with a big caveat: even if your card company can’t see what you’re spending, Net1 can – plus it has to comply with local money laundering and FICA rules to prevent large anonymous transactions.

“Two of the founding principles of VCPay are privacy as well as security,” he says, “Whilst there are the likes of POPI etc. to protect consumer data, clearly if we had to ever compromise privacy or security, our value proposition would in turn suffer considerably and thus we can guarantee that this would never happen.”

Belamant says that under South African law, spending data has to be held on file for three to five years. After that, he says, it will be destroyed.

There is one other, hugely important, area where the card could be enormously beneficial to South Africans and other countries of a similar income level: banking the “unbanked”.

“The reason a lot of mobile money solutions don’t take off,” says Belamant, “Is mostly one of interoperability. Getting money into virtual wallet or M-PESA like system is easy, getting cash out is often very hard. You have to use the right sort of cash machine, for example.”

Because VCPay is based on credit card clearance systems, people can get access to money transferred into their wallet anywhere that currently does cashback.

Belamant does know what he’s talking about. Historically, Net1’s main business has been handling payments for the SA government, so it has a lot of experience working with point-of-sale vendors to allow benefit recipients to draw money at supermarket kiosks. It also has a large payroll system which currently allows corporates to pay workers using plastic cards instead of cash, which again can be converted to money at supermarket tills.

Reducing the amount of cash people have to carry around also improves physical security, and has long been considered a key benefit of mobile money for the poor. One less obvious benefit is that people buying sub-R500 smartphones will be able to actually use features like App Stores without a bank account too.

It gets even better: theoretically, because VCPay is compatible with NFC payments it should also be useable on the mass transit payment system that will unify etickets for Rea Vaya, Gautrain, Metrobus, MyCiTi bus and taxis as its introduced over the next few years.

When it’s formally launched in a few weeks time, VCPay will be a smartphone app on Android, BlackBerry and Apple handsets, but there’ll be a USSD version and a J2ME app for dumb and feature phones too. So someone without a bank account can request a card worth, say, R100 and they’ll get back a single use MasterCard number, expiry date and CVS code via SMS – which they can then use to withdraw cash or pay for goods. It’s the flexibility of using existing standards which makes it potentially more useful than other mobile money methods.

Even though they aren’t common, single use credit cards aren’t actually new – VCPay has been in beta versions on the App Store and Google Play since 2012. But there is about to be a big push to raise awareness and encourage their use. VCPay will be relaunching later this year, with a new beta scheduled for around August and a ‘hard’ launch sometime closer to Christmas.

So we’ll be able to judge whether or not Net1 lives up to its lofty ambitions soon.